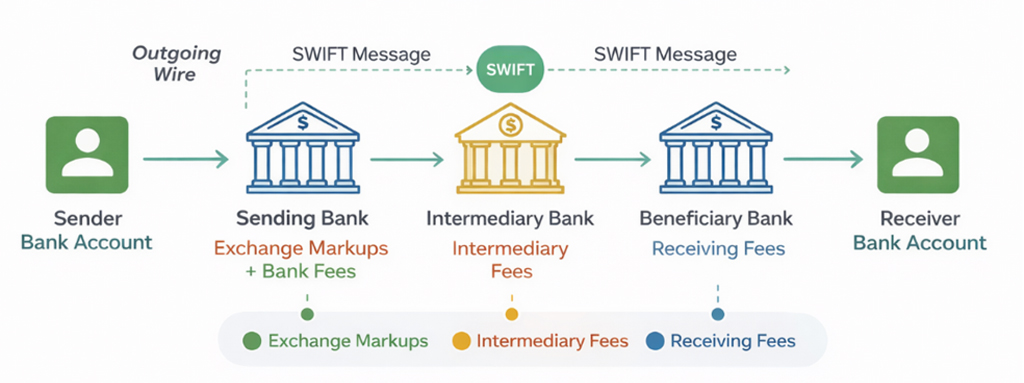

To understand this, you need to see the mechanism. An international bank transfer doesn’t go straight from sender to receiver. It passes through different banks, each adding its own charges on the way. Exchange rate markups, receiving banks, and intermediary fees can all add up to the final amount.

The diagram below shows how a single bank international payment moves through the system and where extra costs quietly appear:

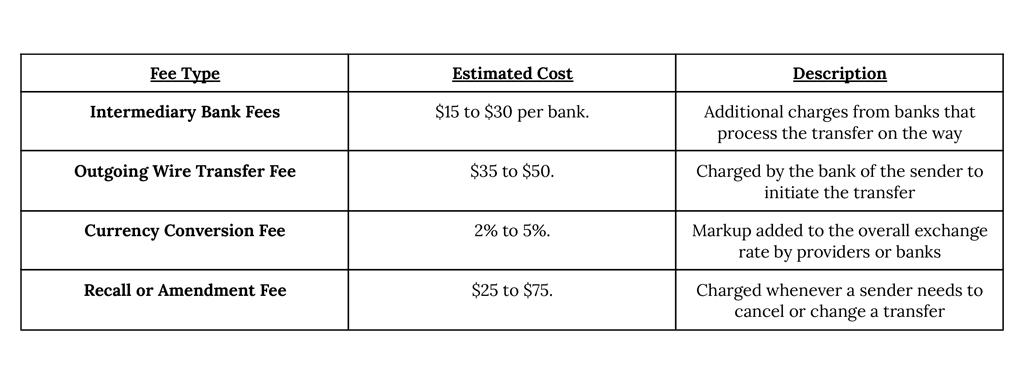

When a bank processes an international wire transfer, some fees are evidently stated. And these are the costs businesses expect already. Depending on the region or bank, wire transfers can involve multiple fees, including:

These bank charges for international payments are disclosed during the transfer process and are listed in fee schedules, too. When they’re high, it’s not a problem as long as there is transparency. Therefore, it only gets tricky when you can’t see yet: the hidden costs.

These bank charges for international payments are disclosed during the transfer process and are listed in fee schedules, too. When they’re high, it’s not a problem as long as there is transparency. Therefore, it only gets tricky when you can’t see yet: the hidden costs.

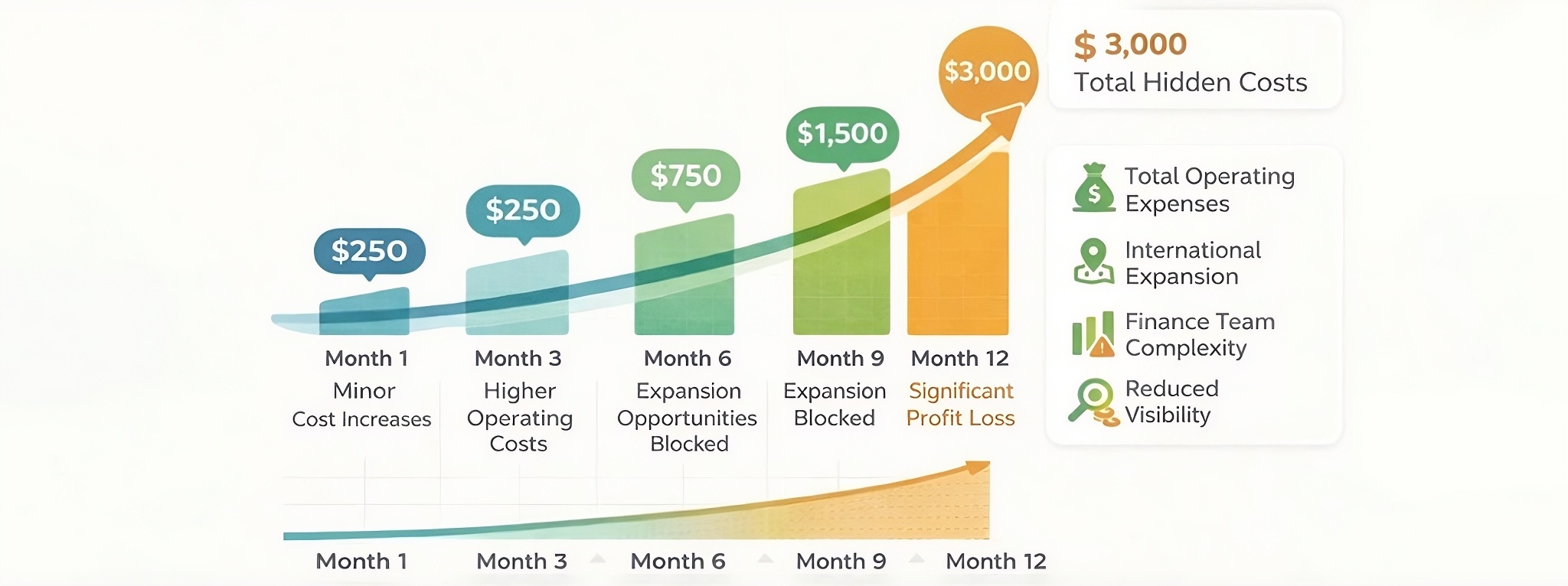

Hidden bank transfer fees seem minor on a single transaction, but their long-term impact is substantial. With time, businesses begin to face issues like:

- Higher total operating expenses

- Difficulty expanding international operations

- Complicated reconciliation for finance teams

- Reduced visibility across regions and currencies